The competition in today’s US insurance market is tough, with around 6000 businesses operating in this sector, according to the Insurance Information Institute. To beat this competition, the industry is shifting from standalone machine learning models to integrated AI ecosystems and LLM-driven systems. Insurers are investing in solutions that deliver measurable ROI across underwriting, claims, and customer experience.

In this article, read about machine learning and AI in insurance. Since the insurance industry has grown an immense appetite for data during the past few years, explore how ML can help your company unleash the potential of this data, process, and use it right.

What is machine learning in insurance?

When it comes to machine learning insurance, we’re basically talking about extracting knowledge from insurance data. According to IBM, ML can be defined as,

A subfield of artificial intelligence (AI) and computer science that focuses on the use of data and algorithms to imitate how humans learn, gradually improving its accuracy.

Deriving from historical data, an ML algorithm can learn on its own from claims data, customer behavior patterns, risk indicators, etc. and make predictions and conclusions without being explicitly programmed. So an ML model generates the results as accurately as possible, and it’s important it was fed with enough quality data.

In practice, this means insurers can:

- Assess risk more precisely during underwriting

- Detect fraud earlier by identifying anomalies in claims

- Optimize pricing based on real-time and behavioral data

- Predict customer churn and personalize engagement strategies

Machine learning plays an important role in transforming insurers into data-driven organizations. It allows companies to operationalize the vast volumes of structured and unstructured data, from policy records to claims notes and IoT inputs, and turn them into actionable insights.

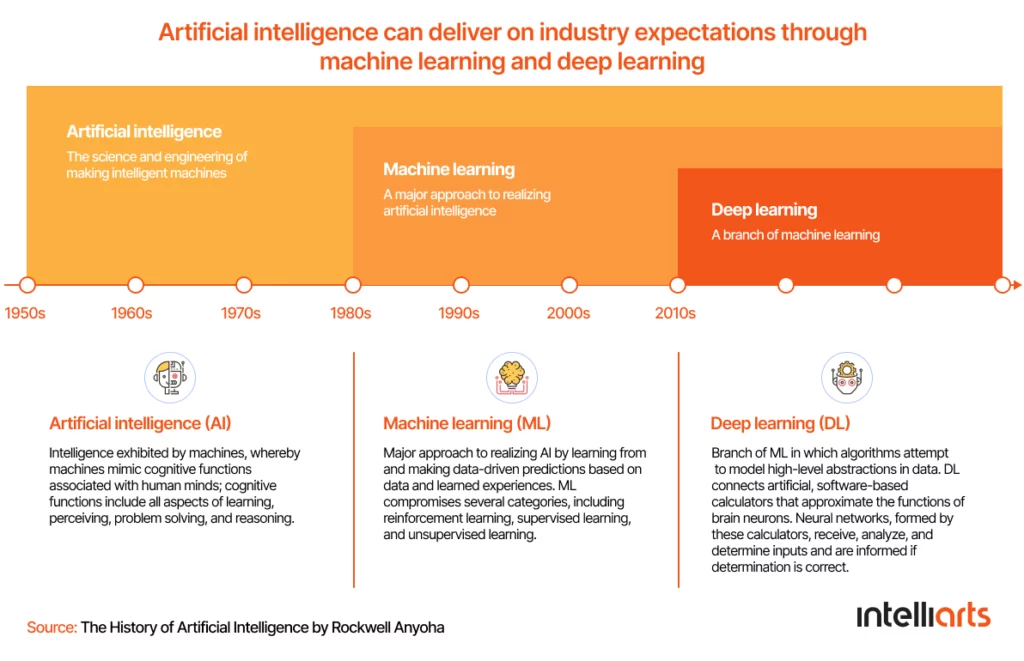

It’s also important to distinguish between machine learning, broader AI systems, and deep learning. While both belong to computer science, AI is a broader concept than ML that is designed to simulate human thinking capability and behavior. From a business perspective, both AI and ML can help you conduct business operations better, with more accuracy and lower spending.

The major difference between machine learning and deep learning lies in how the data gets presented to the machine. While traditional ML algorithms rely on structured data, deep learning can deal with massive amounts of both structured and unstructured information working based on the multiple layers of artificial neural networks. This is particularly valuable in insurance use cases like damage assessment, document processing, and medical data analysis.

What problems does machine learning solve in insurance?

Insurance and insurtech companies operate in a data-rich but decision-heavy environment, where inefficiencies directly impact loss ratios, operational costs, and customer experience. Machine learning can address several core challenges in the industry:

Fraud

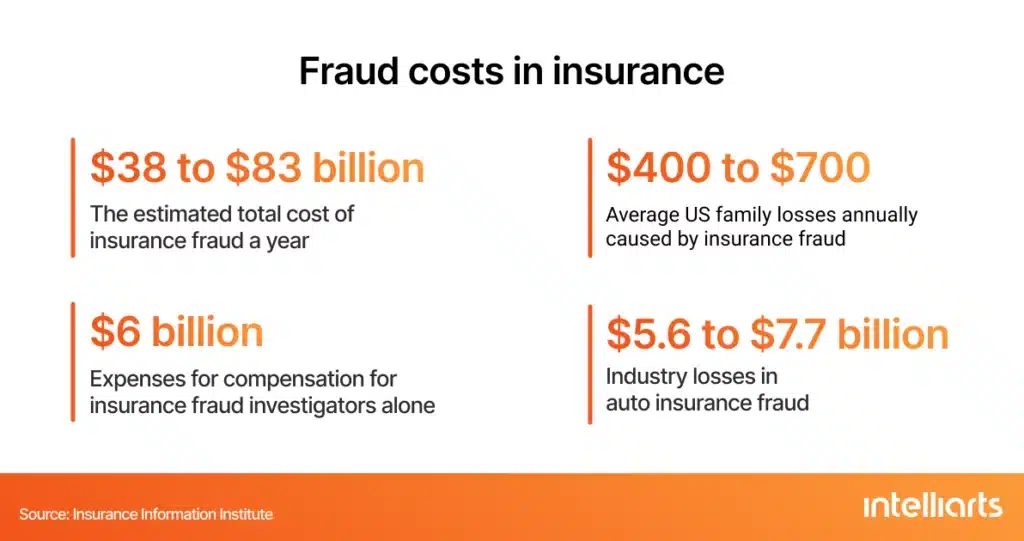

As probably the most challenging task in insurance, fraud detection makes insurance companies lose $80 billion annually, according to the Coalition Against Insurance Fraud. And while businesses are thinking about how to deal with fraud, malefactors are using this time to make up new fraudulent schemes and patterns. Also, this situation makes insurers add costs to premiums and increase prices from 10 to 20% on average, which puts an extra toll on customers.

ML models detect anomalies across claims, transactions, and behavioral patterns, enabling faster and more accurate identification of suspicious activity.

Risk

Underwriting is an important part of insurers’ daily work when a company calculates the risks of insuring someone’s business, assets, or life and picks up the right price for this deal. Traditional risk evaluation relies on static rules and limited datasets.

In contrast, ML-enabled risk management systems allow insurers to speed up and facilitate underwriters’ work. A simplistic example of ML in underwriting includes making decisions on how deeply to investigate the case, e.g. full vs. simplified underwriting or whom to assign the case, e.g. junior vs. senior specialist.

Pricing

A traditional price optimization approach means accommodating GLM (Generalized Linear Model) to historical claims and premiums. GLMs are traditionally used as the main pricing technique, but this conventional approach:

- Doesn’t take into consideration the changeability of insurance pricing. Pricing uncertainty in this sector is high because of constant changes in claims procedures and regulatory requirements

- Doesn’t work in certain circumstances. Taking the same GLMs approach, the result — quoted premiums — can differ from one insurer to another. The study conducted by the Institute and Faculty of Actuaries proves that even for an ordinary risk, this difference can reach up to $1000

Unlike GLM, ML makes possible dynamic pricing. So how can you implement ML in insurance for premiums? Using ML for price optimization brings more accuracy and flexibility to pricing. For one thing, insurers can adjust prices dynamically, for example, by reacting timely to market fluctuations. For another, companies no longer need to orient on industry benchmarks but can make use of predictive models to set an effective price for each premium.

The major benefit of ML-based pricing models is an opportunity to include a variety of variables in the premium, with different levels of impact. ML algorithms discern patterns from data, integrate additional sources and channels (even alternative ones, such as previous claims or social media), and notice trends and new demands at early stages.

In the case study of AXA, a global insurer giant has tried using deep learning techniques to optimize its pricing. The company knew that 7 to 10% of its customers cause a car accident annually. While most of these accidents weren’t serious and cost little to the insurer, 1% of these made up large-loss cases with huge payouts.

As you might expect, AXA wanted to predict those large-loss cases to improve their pricing and cut costs. For this purpose, the company produced an experimental neural network model and entered 70 different risk factors into the model. Eventually, AXA achieved 78% accuracy in their predictions and improved their pricing a lot.

Claims inefficiencies

From claims registration to investigation, adjustment, and settlement, handling insurance claims also takes lots of time for insurance agents. Manual claims processing is slow, error-prone, and resource-intensive. ML and AI in insurance can speed up and automate these processes and, hence, reduce the time spent on claims processing and improve customer satisfaction.

Key applications of machine learning in insurance

Let’s explore how machine learning is applied across the insurance value chain.

Underwriting & risk assessment

Of course, AI and ML cannot entirely replace manual risk assessment in the insurance sector. Still, using underwriting automation AI can increase operational efficiency and intelligent decision-making in a range of ways:

- Automating submission triaging

- Streamlining submission processing

- Assessing risks more accurately

- Predicting potential failure rates and other operational risks

- Optimizing rates for premiums

- Improving coverage recommendations

Business impact: Faster decision-making, improved loss ratios, and increased underwriting capacity.

Example in real life

A good example here is the success story of one global reinsurer, i.e. a company that provides financial support to insurance companies. Using historical and geospatial info, this organization built an ML algorithm to analyze the risk of floods in the area.

The implementation of the ML-based system allowed the reinsurer to:

- Reduce time spent on underwriting by ten times

- Model what to expect from the market in the future with 80% accuracy

- Increase case acceptance by 25%

Read about ML in underwriting efficiency in more detail.

Fraud detection

Since ML algorithms work great for anomaly detection and classification of large datasets, companies rely on machine learning for insurance fraud detection. ML detects patterns and analyzes consumers’ behaviors, for example, in transaction methods. If it notices any abnormal activity, it warns the insurer immediately.

With ML, insurers can detect fake and duplicate claims, and we’re not speaking about “exact matches” only but more complex cases. Add here also the frequent fraudulent cases of upcoding in medical bills and overstated repair costs in auto insurance.

So, here’s why you’d better choose insurance fraud detection machine learning:

- It identifies potential frauds faster and more accurately

- Next to structured data, ML algorithms can analyze non- and semi-structured data, including claims notes. This contrasts ML to traditional predictive models, which limit insurers to using structured data only

- ML allows insurance and insurtech companies to add alternative data sources such as public data or third-party IoT, which improves fraud detection results

Business impact: Reduced fraud losses, lower investigation costs, and faster claims approval for legitimate customers.

Example in real life

Before implementing an ML-based predictive fraud detection system, Anadolu Sigorta, the Turkish insurance company, wasted two weeks manually checking claims for fraudulent activity. As the company processed 25,000 to 30,000 claims a month, the costs were high.

After switching to a predictive system, Anadolu Sigorta became able to detect claims in real time. So, no wonder that it improved its ROI by 210% in one year only. Its total cost savings, thanks to fraud detection and prevention, included $5.7 million.

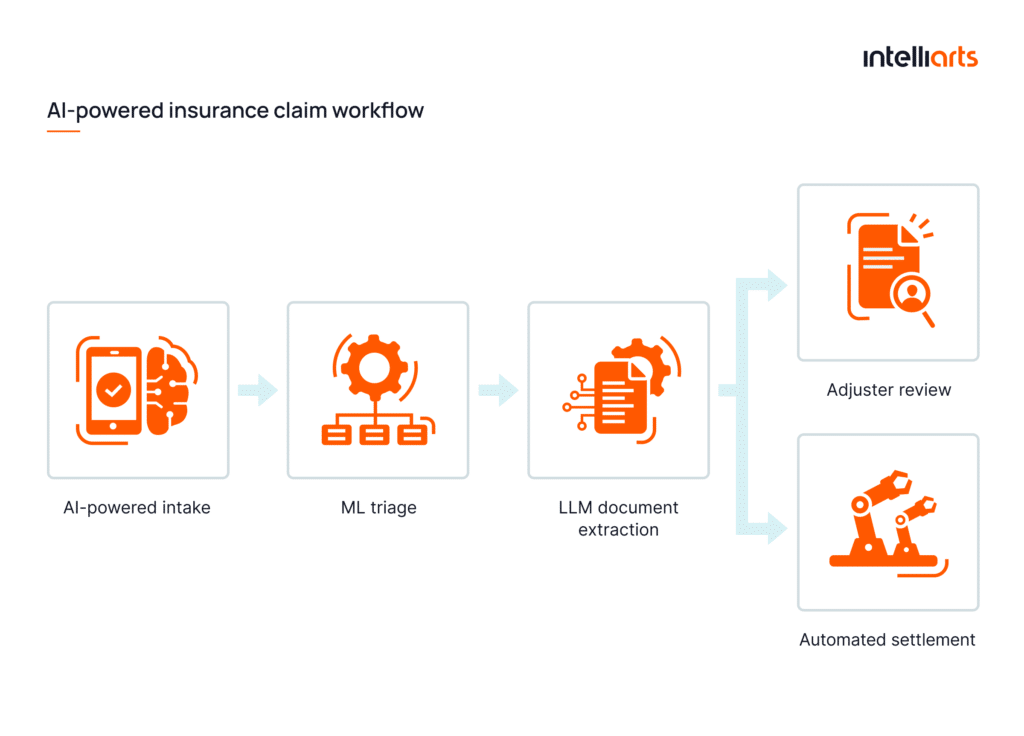

Claims processing automation

Claims processing is rapidly evolving from rule-based automation to AI-powered, end-to-end intelligent workflows.

How can ML and LLMs optimize claims processing?

- By claims registration: The typical claims registration process is time- and data-intensive. ML can provide insurers with analytical insights on how to remove these operation inefficiencies.

- By smart claims triaging: As part of modern insurance claims processing AI, ML is also useful in scoring and triaging risks. If an ML system learns based on past experience, it will be able to prioritize insurance claims faster and more accurately.

- By claims volume forecasting: A typical stumbling block in an insurance practice is to set premiums before signing any insurance contract. An insurance agent, in this case, has to go through lots of manual work and make predictions about the number of claims occurrences and approximate claims amounts. With an ML system in place, the forecast for individual claims will be less error-prone and take less time. As a result, this can decrease the overall claims settlement time and improve customer experience.

- By smart auditing: Using ML algorithms in claims audit improves the quality of audits. Technology helps to identify only those claims that are indeed incorrect and need review. A technical audit can complement these efforts by evaluating the efficiency and security of the technology systems in place.

- By automated damage detection (computer vision): Car insurance companies can benefit from computer vision and automated damage inspections. With AI-based image processing, a customer can upload a photo of the damaged parts of the car, and the system processes the photo automatically. On the way out, both the insurer and the customer receive a detailed report covering which parts are replaceable and repairable (and which are not), together with the approximate estimate for the repair. This reduces the need for manual inspections and speeds up claims processing.

- By generative AI claims summarisation: Large language models (LLMs) can automatically summarize lengthy claims documents, medical records, and adjuster notes into concise, structured insights. (Check a list of LLMs to dive deeper into the topic.)

- By conversational claims support: AI assistants provide real-time, conversational interaction with policyholders throughout the claims process. They can guide users through claim submission, answer questions, collect required information, and provide status updates. While this improves customer experience as they don’t wait long, AI virtual assistants also reduce agent workload.

- Other use cases, including ML-powered auto-adjudication and automatic detection of fraudulent claims.

Business impact: Shorter settlement cycles, reduced operational costs, and better customer experience.

Examples in real life

Intelliarts built a car damage detection solution, which is composed of two separate AI models. One of them indicates the damage, and the other identifies the affected parts. The outcomes are then compared against similar cases in a prepared image database to provide the customer with repair cost estimates.

Also, Liberty Mutual is using an ML-based mobile app, where their customers involved in car accidents can upload photos of their damaged car right at the crash site. Trained with thousands of car accident images, the ML model will automatically calculate repair costs. In real time, the customer can also settle a claim using the same app.

In one of our previous posts, we have already written about what is the role of computer vision for car damage detection.

The Fukoku Mutual Life handles claims data with the help of AI and deep learning. Technology helps the insurer automatically find and access medical documents related to the case as well as calculate the pay-offs. As a result, the Japanese insurer can now boast of a 30% increase in productivity and cost savings of around $1 million a year.

Predictive analytics for customer retention & personalization

Machine learning also has lots of potential for customer acquisition and retention, as well as customer service in general.

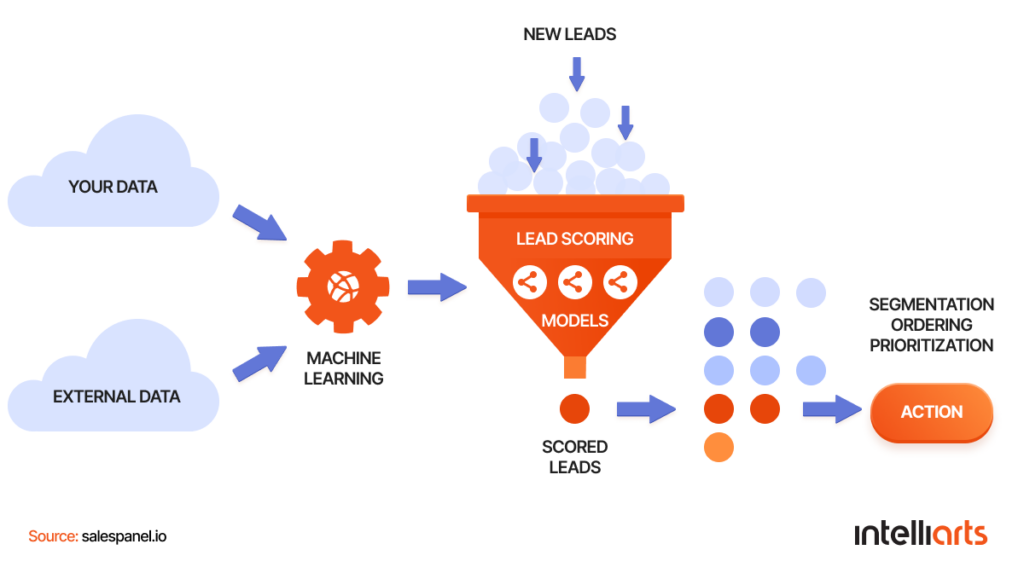

First and foremost, insurance and insurtech companies can consider implementing ML-based insurance lead management systems. By extracting valuable insights from lead data, ML helps insurers with lead analysis and classification. So, companies can choose quality leads and don’t waste time on those with low conversion rates.

A powerful insurance lead management system can also help to calculate the sales threshold by analyzing various important factors, such as lead revert time, link clicks, or web visits. When a lead approaches the industry benchmark, agents will know it’s worth a cold call or a message.

Secondly, ML is very effective at predicting the churn rate. In insurance landscapes, a lapse occurs whenever the customer stops paying the premium, and the contractual grace period expires. ML can help to detect early churn signals and recognize at-risk customers. This way, agents will have enough time to interfere and talk to clients about the reasons for unpaid premiums and negotiate terms of payment.

Another benefit here is the ability to segment customers based on the lapse risk. So insurance companies can use the factor of solvency when issuing policies.

Thirdly, there is personalized marketing as another great use case of machine learning in insurance. Customers in insurance (as anywhere else) would like the services to match their specific needs and requirements. ML can help insurers deliver personalized and relevant experiences.

For example, VahanBima is a leading provider of insurance services in India. The company predicts CLV using a linear regression algorithm and then uses the model results to allocate resources better and target customers with 100% personalized experience offers.

By extracting valuable insights from demographic data, customer behaviors, attitudes, interactions, and lifestyle details, ML algorithms provide insurers with insights to exploit in their marketing initiatives:

- Personalized offers and policies

- Loyalty programs

- Insurance packages

- Pricing

- Messages

Probably the best example is insurance product/policy recommendations. Based on volumes of historical data, AI algorithms can analyze customer profiles and provide the most suitable policy offers out of those available, which will raise the chance of a successful sale. For example, Accolade offers personalized insurance services with the help of machine learning in insurance and helps patients choose the most relevant and cost-effective health coverage. Now the company reportedly has over 1.1 million customers.

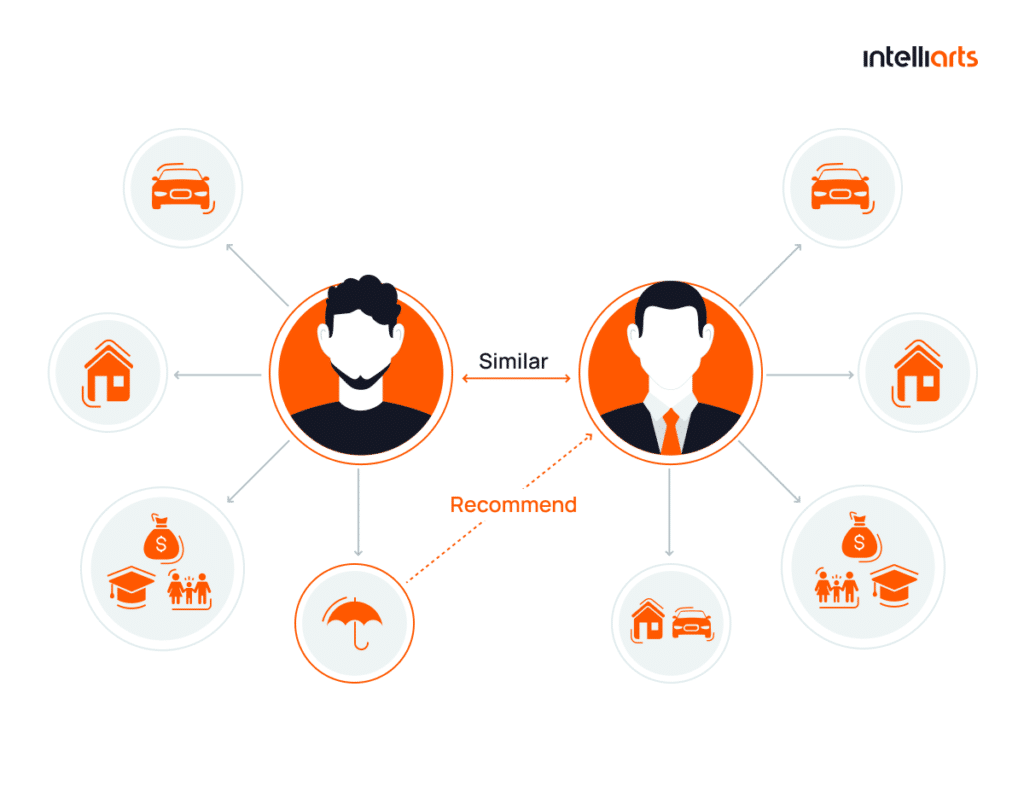

An interesting approach is to use collaborative filtering for personalized offers. This means that an ML system suggests a product to customers based on their similar risk profile and/or purchase history to other customers who have bought this product earlier.

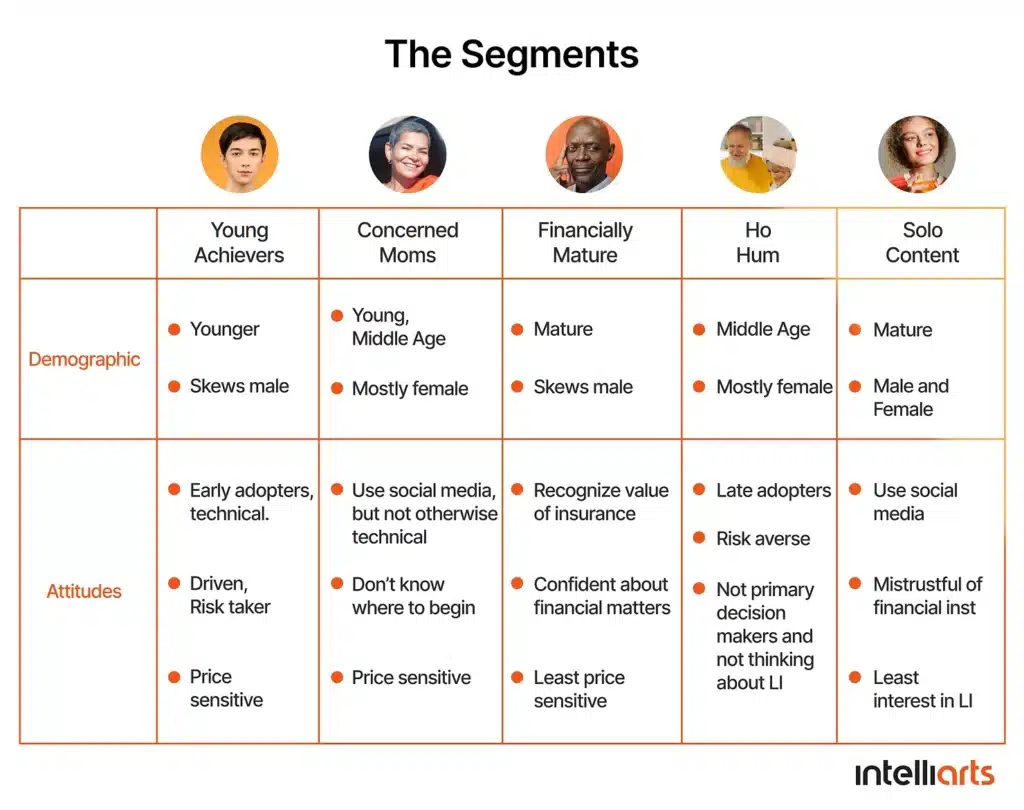

Last but not least, ML algorithms can come in handy in customer segmentation. Analyzing important data, such as customer income, age, gender, and location, ML classifies customers into different groups. It can also seek patterns based on more complex variables, such as behaviors or personal preferences. Using these conclusions, an insurer then develops specific attitudes or uses marketing strategies to target different customer segments.

Business impact: Higher customer lifetime value (CLV), improved retention rates, and more efficient marketing spend.

Examples in real life

The Intelliarts team built a predictive scoring model that could forecast the probability of how likely the lead would buy a policy. With this system in place, insurance agents could call leads with high scores first and leave those leads with low scores for later or skip them entirely in case of a lack of resources.

The business value was far above the expected. After only a few months in production, the model helped to cut off approximately 6% of non-qualified leads, which resulted in a 1.5% profit increase. In the most successful months, the customer noticed a 2.5% increase in profit.

Another example is the case of a life insurance company, MetLife. The company decided to take a data-driven approach to customer segmentation. At the time when insurers used ML solely for risk mitigation and underwriting, MetLife centered on ML to foster their go-to-market strategy and achieved great results.

ML algorithms helped the insurance company to understand the customers’ needs, behaviors, and attitudes better and, hence, maximize their competitive advantage. Later, MetLife summarized this experience as “the most significant change to their brand in over 30 years.”

Since an ML model can look at and extract patterns from millions of data points at once, it provides custom recommendations and insurance packages to create a robust user experience in the domain.

NLP for insurance document extraction

Going through tons of text documents like health records, financial reports, claims history, and even mental health EHR data takes at least half of a working day for those in insurance. No need to say that these tasks are monotonous and tiresome but require lots of accuracy.

Traditionally, NLP combined with OCR has been used to extract key fields from these documents and convert them into structured data. ML-based data extraction in insurance such as with the help of EMR software can further streamline this process, reducing manual workload and improving accuracy.

- By scanning through texts automatically, ML algorithms retrieve core words and/or phrases from unstructured insurance documents. Even better, they can identify synonyms or related words, e.g. searching for a “pet” when you’re looking for a dog.

- Optical character recognition (OCR) also enables image to text conversion, allowing insurers to recognize handwritten and printed texts, process documents faster, and solve operational inefficiencies.

- NLP insurance document processing helps to generate automatic summaries of documents so insurance agents won’t need to read 100-page financial reports.

- Finally, AI for data extraction allows forgetting manual re-typing. When paired with computer vision in insurance, it can accurately render every single pixel and translate the information if needed. This is especially useful when it comes to customer onboarding and claims management, helping to extract customer information in the blink of an eye.

Advanced NLP models mark the transition from data extraction to contextual understanding and, hence, automation of more complex workflows in the insurance industry. What’s more, NLP serves as a foundation for LLM-based systems, which further extend these capabilities with summarization, reasoning, and natural language interaction and which we’ll talk about next.

Business impact: Reduced processing time, fewer human errors, and scalable document handling.

Example in real life

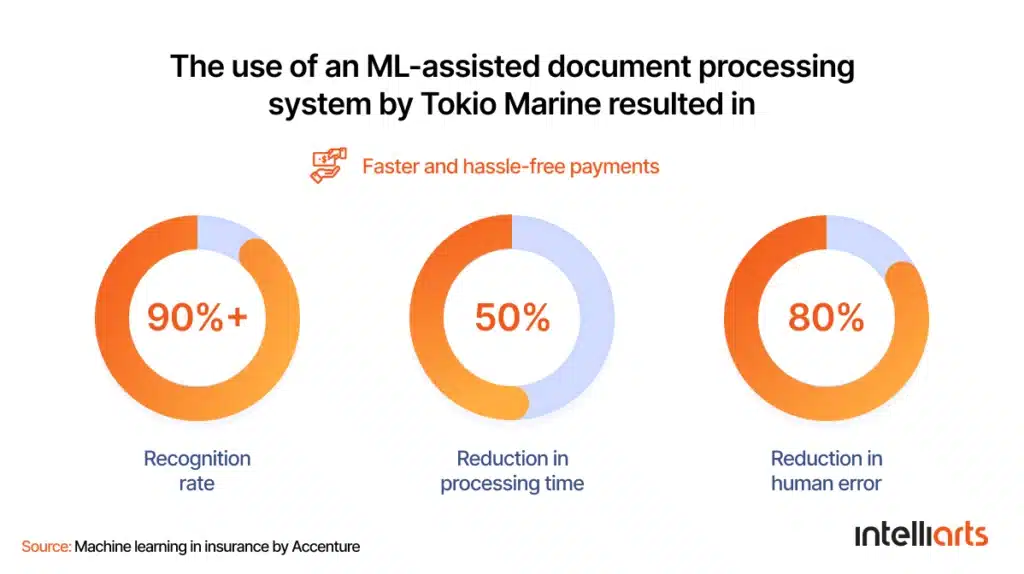

Tokio Marine uses an ML-based OCR service to handle claims. The system allowed the company to reduce human error by 80% and processing time by 50%.

How LLMs are transforming insurance

While machine learning has long powered predictive analytics in insurance, the industry is now shifting toward LLMs that can understand and generate human language. This helps to unlock new levels of automation and efficiency in insurance.

From NLP to LLMs in insurance: What changed?

Traditional NLP models like BERT or RoBERTa are primarily used for classification tasks, for example, tagging claims, detecting sentiment, or categorizing documents. These models are effective but limited to predefined outputs.

LLMs in insurance, in contrast, focus on generation and reasoning. Instead of just classifying data, they can:

- Summarize complex claims documents

- Generate responses to customer queries

- Extract and structure key information from unstructured text

- Support decision-making with contextual understanding

Real-world LLM use cases in insurance

Claims summarization and processing

As partly mentioned, LLMs can speed up claims workflows by summarizing large volumes of unstructured data, such as medical records, adjuster notes, and claims history, into concise, decision-ready insights. This reduces manual review time for claims handlers. Generative AI claims summarisation also improves decision consistency, especially in complex or document-heavy scenarios.

Zurich Insurance Group is leveraging generative AI to streamline complex claims and policy analysis workflows. In multinational insurance programs, often involving thousands of policies across jurisdictions, LLMs help internal experts compare, summarize, and verify coverage in a single language.

With over 8,500 multinational programs and 56,000 policies across 200+ countries, Zurich uses GenAI to process large volumes of documentation in the limited time required for manual review. This improves both speed, especially in complex claims data, and reduces manual workload for specialists.

We’re excited about the future possibilities that GenAI brings. It offers incredible opportunities to reduce manual workload and allow our people to spend more time in the areas they can add most value. This will ultimately drive better insights and service to our customers and brokers. – Sierra Signorelli, CEO @ Zurich Commercial Insurance

Conversational AI and customer support

LLM-powered assistants significantly upgrade traditional chatbots. Instead of scripted responses, they produce natural, context-aware conversations. AI assistants, in this case, can help customers with claims submission, answering policy-related questions, and providing real-time updates. They can also support content delivery, including instructional video production, to guide users through complex insurance processes.

A prolific example is the use of TextQBE by QBE North America, a global insurance leader. This virtual assistant helps the company answer simple questions from customers about deductibles and process photos of receipts and other documents.

Customer satisfaction scores through the service have averaged 4.6 out of 5 – many with comments such as “great customer service, fast and friendly,” answered all my questions. – Eric Sanders, Senior Vice President @ QBE North America

Intelliarts has lots of experience with ChatGPT and other LLM chatbot development. Read this case study on a data extraction solution based on ChatGPT to get more details.

Document understanding and data extraction

While ML and OCR automate document processing, LLMs add a critical layer of contextual understanding. They can extract key entities (e.g., damage type, cost, policyholder), identify relationships, and generate structured outputs. Again, this helps eliminate manual data entry and speed up workflows.

Explore text generation models in insurance in one of our readings.

Adding the LLM layer: Retrieval-Augmented Generation (RAG)

To ensure accuracy and compliance, insurers are increasingly adopting Retrieval-Augmented Generation (RAG). RAG combines:

- Internal knowledge bases (policies, underwriting rules, claims history)

- External data sources

- LLM reasoning capabilities

This technology strengthens LLMs in insurance even further. RAG insurance knowledge retrieval allows systems to generate fact-based, context-aware responses based on company data. This is especially useful in a highly regulated environment. Some examples include:

- Claims assistants referencing policy terms in real time

- Customer support bots providing compliant, personalized answers

- Internal copilots helping agents navigate complex documentation

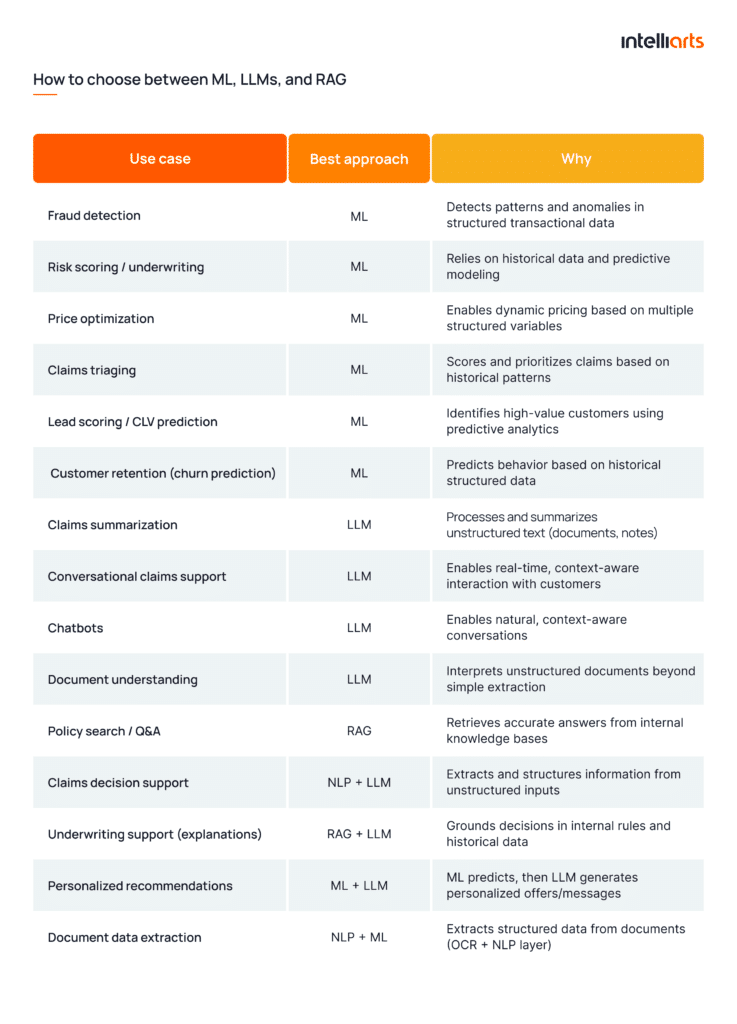

How to choose between ML, LLMs, and RAG

From our customers’ experience, we noticed that, as insurers adopt more advanced AI capabilities, a common challenge they face is how to choose the right approach for a specific business problem. Machine learning, LLMs, and RAG are indeed not interchangeable because they solve different types of tasks.

Summarizing our 6-year experience working on ML projects, we can say that at a high level:

- ML is best for prediction based on structured data

- LLMs helps with understanding and generating unstructured text

- RAG enables accurate, context-aware answers using internal knowledge

So the key is to align the technology with the nature of your data and the decision you need to make. Use the decision framework below to choose between ML, LLMs, and RAG in insurance:

One pro tip from the Intelliarts team is to combine these technologies into layered systems instead of choosing one approach. This is how to use them in practice most efficiently:

- Use ML models to predict risk, fraud, or customer behavior

- Apply LLMs if you need to interpret documents and interact with users

- Add RAG to base your outputs in internal policies and improve accuracy

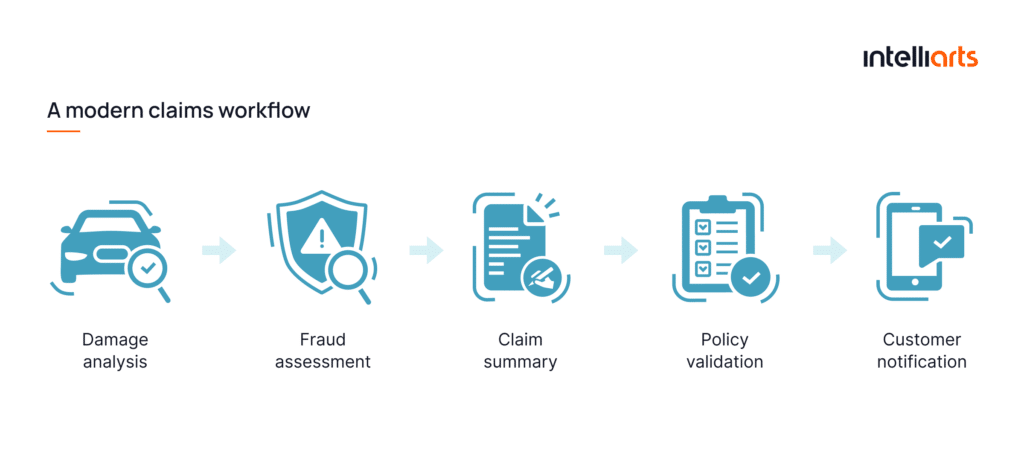

For example, a modern claims workflow can combine computer vision for damage detection, ML for fraud scoring, LLMs for summarization, and RAG for policy-aware validation.

How to implement ML in the insurance business

Building reliable AI in insurance follows a structured process. But leading insurers go further by embedding these steps into scalable systems.

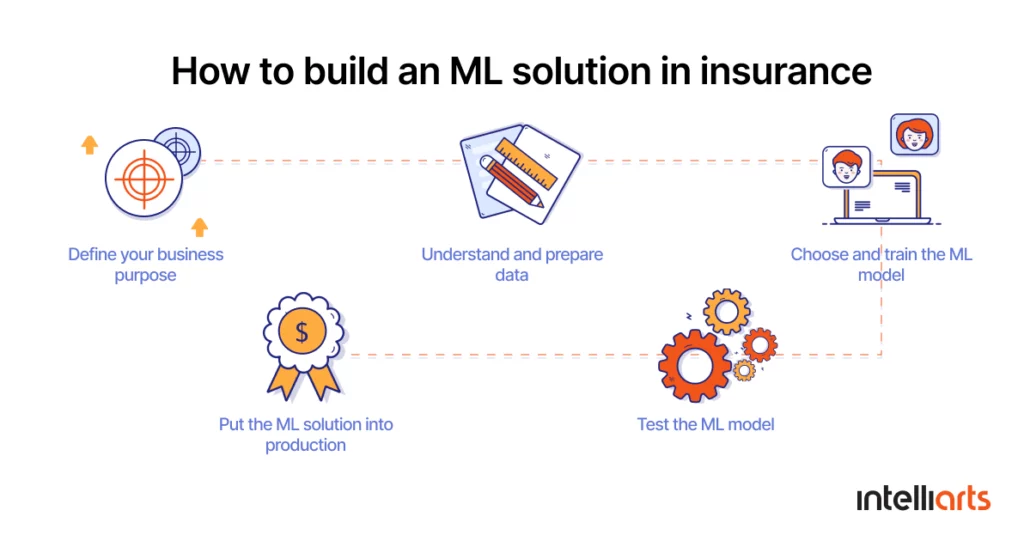

1. Define your business objectives

A good idea for getting started with ML is to consider what business tasks you need it for. Earlier we mentioned the key use cases – go through them and think about which are relevant to your company. Then, prioritize the tasks based on your biggest pain points and those that are only nice to have.

Try to be as specific in your objectives as possible. You can also seek the consultation of professional data engineers who have industry expertise in insurance.

2. Understand and prepare data

Getting quality insurance data, as well as the efficient amount of data are a top priority for building a reliable ML solution. Under the supervision of expert data scientists, you identify and understand the data you own now or need to collect in the future.

Most insurance companies have repositories of existing data (think about your historical claims data or policy data). Even if you don’t have enough raw data, a professional ML team can assist you with data collection, advising on the best types of data, formats, or ways of storage. Data engineers can also back up your business with synthetic data if needed.

For those interested in data collecting and contributing to this crucial phase of the process, there are abundant opportunities on Jooble to explore.

After data collection, data scientists will also need to invest time in data exploration to find patterns in data, investigate relationships between variables, and determine how these will affect the outcome. Data visualization can be really helpful at this stage. Also, data cleansing and validation, as well as data structuring, may be needed to process the data the most efficiently.

3. Choose and train the ML model

This is when the ML model is actually being built. Data scientists need to explore different ML algorithms and choose the ones most suitable for your business problem. Then, these algorithms are trained — the model is fed with training datasets, the results are evaluated, and engineers fine-tune model parameters until they get high accuracy.

4. Test the ML model

Testing is a critical step in building an ML-powered solution. Here data engineers under the guidance of the insurance company check whether the ML system works as planned and whether the results are satisfying enough (maybe the model needs more training).

5. Put the ML solution into production

When the ML model is ready, data engineers can move to machine learning deployment in insurance. Ideally, the ML team should also assist with model monitoring so you can track the results without diving deeper into the technical details. With decent model monitoring, your insurance company will also know when the model needs retraining in case you get new datasets.

Above we described a traditional ML pipeline (Data → Model → Decision → Feedback loop), commonly used in underwriting, fraud detection, and price optimization. In case, you’re planning to build an LLM-based pipeline, your workflow will be the following:

Data → Embeddings → Retrieval → Generation

#1 Data: Collect and prepare structured and unstructured inputs (documents, policies, claims, customer interactions)

#2 Embeddings: Transform data into vector representations for semantic understanding

#3 Retrieval: Retrieve relevant information from internal knowledge bases or external sources

#4 Generation: Produce context-aware outputs (e.g., summaries, answers, recommendations), often enhanced through LLM fine-tuning

This architecture is suitable for document understanding, claims summarization, and conversational AI.

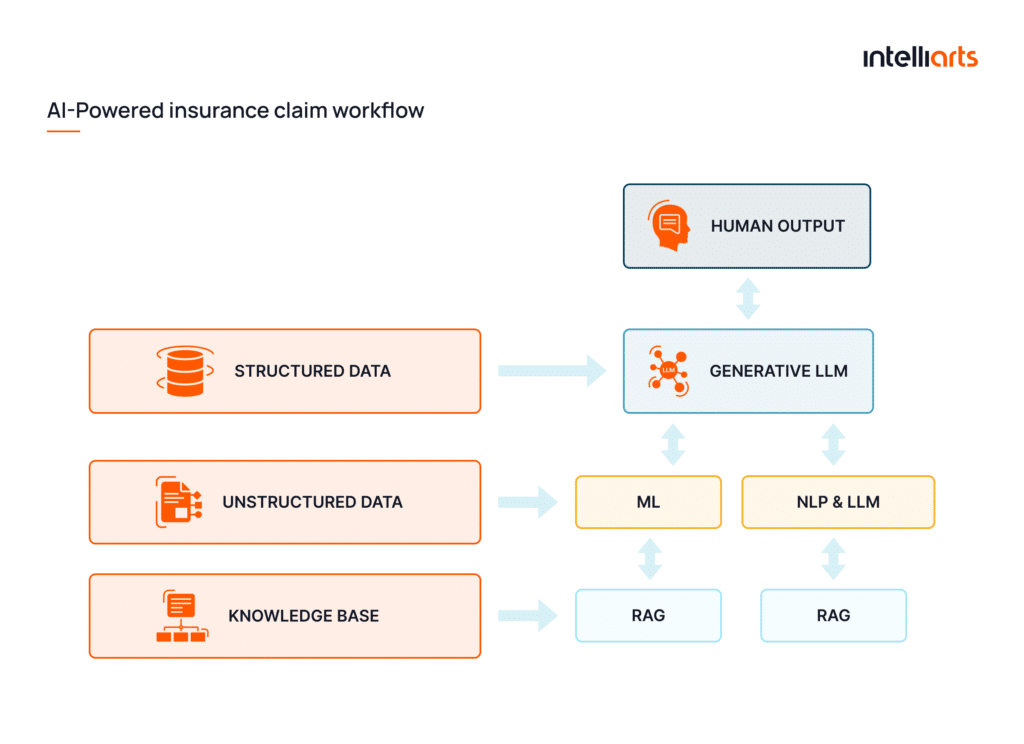

To sum up, modern insurance platforms combine multiple AI layers in their architecture:

- Data layer: structured and unstructured data (claims, policies, telematics)

- ML layer: prediction (fraud, risk, pricing, actuarial modeling)

- LLM layer: language understanding (claims, support, documents)

- RAG layer: knowledge grounding (policies, compliance rules)

- Automation layer: enabling straight-through processing

- Feedback loop: continuous learning and improvement

This layered architecture allows insurance companies to build systems that are efficient, accurate, and compliant at once.

Challenges of implementing AI in insurance

Adopting AI in insurance requires more than building models. It demands a strong foundation in data, compliance, and trust. That’s why there are a number of challenges that insurers have to deal with:

#1 Data quality and availability

ML solutions are data-driven, and the performance of the future ML model largely depends on the data used to feed the algorithms. Yet, insurance data quality is often inconsistent, siloed, and unstructured (e.g., claims documents, medical records).

Without proper data preparation, even the most advanced models will underperform. This is especially critical for use cases like actuarial ML and telematics-based risk assessment, where accuracy directly impacts pricing and underwriting.

What’s more, if the insurer lacks ML expertise, they might not even know what data to collect and where to get started. Paired with a skilled ML team, you can get advice on the best data collection methods as well as create synthetic data if needed.

#2 Regulation and compliance

Insurance AI solutions must comply with strict regulations such as GDPR insurance AI requirements and the EU AI Act for high-risk systems. Many insurance use cases, such as underwriting and pricing, fall under high-risk categories and require transparency and human oversight.

#3 Model explainability and trust

In regulated environments, decisions must be explainable. Whether it’s pricing, underwriting, or fraud detection, model explainability is important to justify outcomes to regulators and customers, and to grant fairness and accountability.

#4 System integration and legacy infrastructure

One of the biggest barriers to AI adoption is integrating new models into existing insurance systems. Legacy platforms and fragmented data sources make it difficult to deploy AI/ML at scale. Successful implementation requires seamless integration with core systems (policy administration, claims management) and alignment with existing processes.

#5 Digital mindset and culture

Adopting ML isn’t enough if your personnel refuse to use it in their daily activities. So, make sure you build a data-driven corporate culture, with clear cooperation between IT and other departments. A good starting point is to organize training sessions to teach the personnel how to use ML to the fullest value.

Future of AI in Insurance

Insurance is a highly competitive industry, especially now when many companies are operating online. A good way for an insurance company to stand out in the competition is to use the benefits of innovative technologies and machine learning in business, in particular.

Today the industry is entering a new phase of transformation powered by:

- Generative AI. LLMs in insurance bring new use cases to the industry, including automatically generating claims summaries and reports, powering conversational assistants for customer support, and producing personalized policy recommendations and communications. This shift allows insurers to move from analyzing data to acting on it in real time. For example, tasks that once required hours of manual review, such as analyzing claims documents or policy details, can now be completed in seconds with LLM-powered systems.

- Autonomous workflows. This means that multiple AI components work together with minimal human intervention. Instead of isolated tools, insurers are building systems that combine computer vision (e.g., damage detection) with ML models (e.g., fraud scoring, risk prediction), LLMs (e.g., summarization, communication), and RAG (e.g., policy validation, compliance checks). For example, a modern claims workflow can look like:

What does this mean for insurance companies? Machine learning in insurance, along with LLMs, is transforming every part of the insurance value chain. The insurers of the future (and you can become one of them easily) are getting value from the abundant insurance data they’re sitting on and use ML to:

- Increase underwriters’ efficiency

- Handle claims faster and in a more productive way

- Detect fraudsters in a few minutes

- Predict potential churners and take measures to retain customers

- Analyze leads more effectively and choose the most promising ones

- Extract valuable insights about their customers to apply personalized marketing tactics

- Segment customers to target them better

- Extract data easily

- Optimize premiums and adjust them dynamically to market changes

Wrap up

In the last decade, the insurance sector has produced and accumulated as much data as ever before. The bad news is that insurers use not more than 10-15% of this data, according to the Accenture study. Using machine learning in insurance can help use the data to which they have access to its fullest potential and improve their business in a range of ways, from fraud detection to risk mitigation to claims processing and price optimization.

Intelliarts combines vast expertise in machine learning and domain knowledge of the insurance industry. We provide technology consulting services, including AI consultation where we can assess your readiness and prepare a detailed roadmap for adopting ML into your processes. Our data science team could then help you with ML implementation.

Want to get started with machine learning in insurance? Or maybe optimize your existing ML system?

FAQ

What is machine learning in insurance?

ML development solutions can bring lots of value to insurance companies. For example, it can help with predicting trends and, hence, better decision-making and cost optimization. Another benefit includes increased customer loyalty thanks to faster and more quality services delivered. Insurers can achieve these via automated claims processing, personalization, and more accurate underwriting services.

What are the most common applications of ML in insurance?

There are many use cases for machine learning in the insurance industry, from automated claims processing to fraud detection, price optimization, and automated risk assessment.

How do LLMs differ from traditional ML in insurance?

LLMs differ from traditional machine learning in that they can understand and generate human language. In insurance, ML is used for tasks like fraud detection or risk scoring. In contrast, LLMs are suitable for claims summarization, document understanding, and conversational customer support.