Machine learning underwriting alters how businesses evaluate risk, assess applicants, and automate decision-making across various industries, from insurance to real estate to fintech. Although traditionally conservative and process-heavy, underwriting is now undergoing a rapid digital transformation powered by AI and ML technologies. These tools have revolutionized underwriters’ daily operations, improving accuracy, reducing the process time, and increasing overall machine learning underwriting efficiency.

From better underwriting risk calculation to automated claims processing, machine learning helps organizations make more data-driven decisions and streamline operations. In this guide, we explain how machine learning underwriting works, where it delivers the most value, and what organizations should consider when building ML-powered underwriting systems.

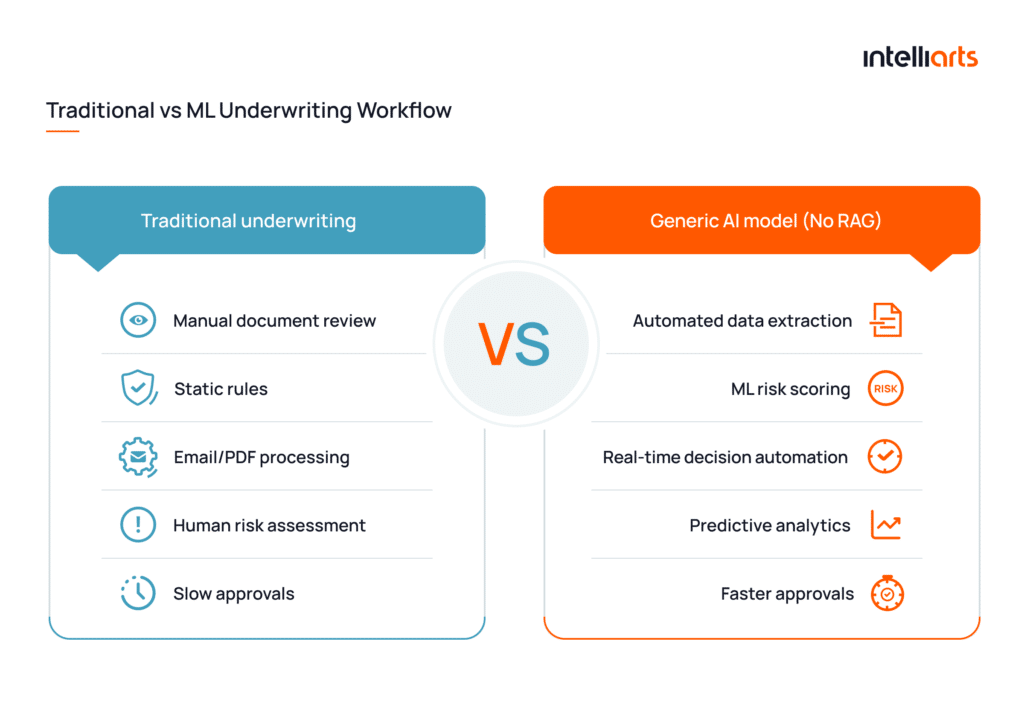

Why traditional underwriting falls short

Across industries such as insurance, lending, real estate, and equipment financing, traditional manual underwriting is associated with piles of physical and digital paperwork, back-and-forth communication between stakeholders, entering and rechecking lots of information submitted into the system. This is without mentioning a cumbersome and time-consuming process of evaluating risk to determine whether to approve a deal — and under what terms.

Manual underwriting workflows typically involve repetitive administrative work: reviewing PDFs and emails, re-entering data into internal systems, verifying documents, and coordinating across multiple stakeholders. Statistics indicate that underwriters spend 40% of their time on administrative and other non-core activities. As application volumes grow, these inefficiencies lead to longer turnaround times and rising operational costs.

Limited data usage creates another major challenge. Traditional underwriting models rely heavily on structured applicant-provided information and static rules, which restricts an organization’s ability to assess risk dynamically. Without access to broader data pipelines and predictive analytics, underwriters may miss important risk signals or pricing opportunities.

Still, the rise of ML and AI technology proves that, in a few years, underwriting as we know it today is doomed to failure. BCG reports that underwriters adopting AI-first operating models can improve productivity by 30% to 40% while significantly accelerating underwriting and claims decision-making processes.

It’s not really surprising if we consider how AI underwriting helps better analyze risks, provide more accurate pricing, and process applications faster and more efficiently. With ML and deep learning technologies, the underwriting process time is reduced to a few minutes (instead of hours or even days) because most activities are automated and data-driven. As Matthew Josefowicz, a technology strategist and opinion leader in insurance, summarizes it,

New technology is allowing underwriters to spend more of their time building and strengthening relationships in the field and, in many cases, acting as the frontline interface of the company with the marketplace.

What is machine learning underwriting?

Machine learning underwriting uses ML models and predictive analytics to automate underwriting workflows such as risk scoring, application review, pricing, and approval decisions. Instead of relying only on static rules and manual assessments, AI underwriting systems analyze large volumes of data to improve decision speed and consistency.

The biggest misconception about machine learning underwriting is that it replaces underwriting expertise. In reality, the most successful systems combine predictive ML models with human judgment and business rules. The goal isn’t full automation — it’s enabling underwriters to make faster, more consistent, and better-informed decisions at scale. – Oleksandr Stefanovskyi, Strategic Technology Partner at Intelliarts

Modern underwriting automation platforms can process applications in real time, identify hidden risk patterns, and support more accurate decision-making across industries including insurance, lending, real estate, and equipment financing. Combined with explainable AI and intelligent data pipelines, machine learning underwriting helps organizations scale operations without sacrificing transparency or compliance.

What is underwriting?

Underwriting is the process of evaluating risk before approving financial or asset-related transactions. It is widely used across industries such as insurance, lending, real estate, equipment financing, and logistics, where businesses need to assess applicants, assets, contracts, or investments before making decisions.

Underwriters analyze factors such as financial history, asset value, market conditions, operational risks, and compliance requirements to determine whether a transaction should be approved and under what terms. As said, as data volumes and application complexity continue to grow, traditional underwriting workflows often become decision-making bottlenecks that slow operations and limit scalability.

How machine learning improves underwriting efficiency

Predictive underwriting helps process applications faster, improve risk evaluation, and reduce operational overhead. Let’s consider real value from underwriting automation:

- Faster decision-making: ML-powered underwriting systems can automatically process applications, extract data from documents, and prioritize submissions based on risk or complexity. In our clients’ experience, this reduced review cycles from days or hours to minutes and allowed underwriting teams to handle larger application volumes.

- Improved risk accuracy: The distribution chain in underwriting can be lengthy, with one submission reviewed by several employees. The more people involved and the more manual work, the lower the accuracy becomes in the submission review. By using machine learning models, businesses can handle incorrect and superfluous data better as these solutions are trained on historical data sources. This can improve the accuracy of your risk assessment.

- Reduced manual workload: Traditionally, underwriting has relied on human expertise, and this is understandable and will remain as it is. Machine learning could “unload” underwriters, taking the most tiresome and repetitive work from them. Instead, employees could focus on more interesting and complex cases of risk assessment. Sofya Pogreb, the CEO at Next Insurance, comments on the current situation in the following way:

We believe with technology and machine learning, a lot of [human underwriting] can be done away with. The percentage of insurance applications that require human touch will go down dramatically, maybe 80% to 90%, and even to low single digits.

- Better customer service: With machine learning, services are delivered to customers faster and more efficiently. This increases customer satisfaction and loyalty. Also, underwriting automation brings more personalization and precision to underwriting. For example, a company can offer personalized vehicle lease or financing terms based on driving data points and personal driving behaviors. Another example is the ability to dynamically update the number and type of questions an underwriter should ask during the application process, depending on the applicant’s profile and prior responses. From our customers’ experience, this can be especially useful in industries like lending, equipment leasing, or commercial real estate.

Key use cases of machine learning underwriting

Machine learning underwriting is no longer limited to insurance workflows. Businesses across lending, real estate, leasing, and financial services use ML models to automate risk assessment and improve decision accuracy. Let’s consider key use cases today:

Lending & credit risk

Problem: Traditional credit underwriting often relies on limited financial data, static scoring models, and manual reviews that slow approvals and may overlook important borrower risk indicators.

ML solution: Machine learning models can analyze broader data pipelines, including transaction history, behavioral signals, cash flow trends, and alternative financial data, to improve credit risk scoring and automate application triaging.

Business outcome: Lenders can accelerate approval times, reduce default risk, and offer more personalized loan terms.

Insurance risk assessment

Problem: Insurance underwriting teams process large volumes of submissions, documents, and risk variables, making manual evaluation time-consuming and inconsistent. Also, underwriters may rely on applicant-provided data only, which could have mistakes and omissions, intentional or unintentional

ML solution: ML systems can assist underwriting with getting information from alternative and more diverse sources and, thus, promote a 360-degree approach to underwriting risk analysis. Machine learning underwriting can help check an application profile against loads of data points retrieved from social media platforms, banking records, publicly available statistical data, and third-party databases. It’s also useful for underwriting fraud detection in insurance, helping identify suspicious applications, inconsistent customer information, and anomalous risk patterns before policy approval.

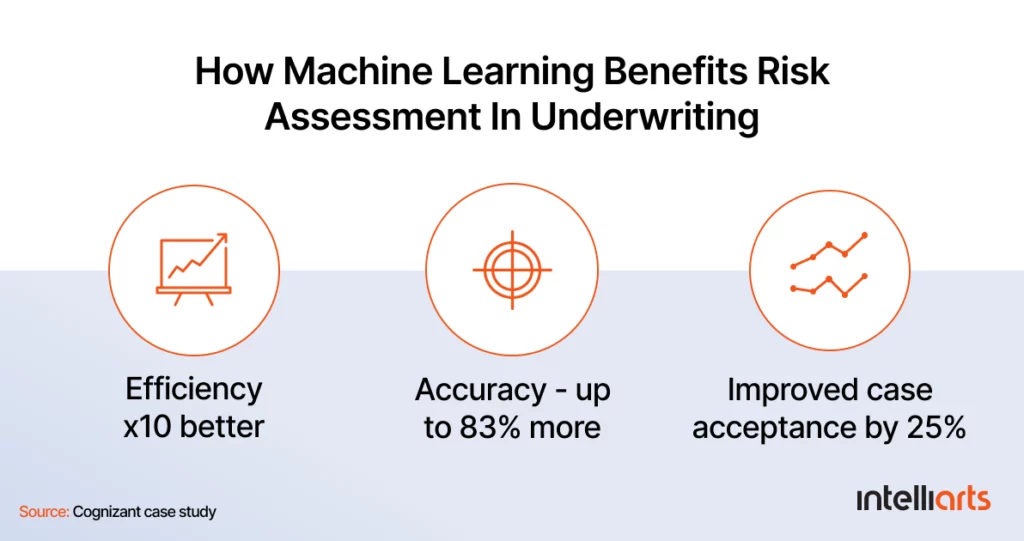

Business outcome: The risk analysis is more accurate. Let’s check the example of one insurance company that used an ML algorithm for predicting the likelihood of flooding in the area based on historical and geospatial data. The adoption of ML technology into the operations allowed the company to increase the accuracy of underwriting services to 83%, generate a 10-fold reduction in throughput time, and increase case acceptance by 25%.

Read about other ML applications across the insurance value chain based on our real-life experience.

Real estate underwriting

Problem: Real estate underwriting requires evaluating multiple variables such as property condition, market trends, borrower history, and asset valuation, often across disconnected systems and data sources.

ML solution: ML underwriting platforms can combine geospatial data, market analytics, computer vision, and historical transaction data to automate property assessments and identify hidden risk factors. For example, ML solutions can help deliver more accurate property valuations by using object recognition to assess the physical condition of a building, the materials used, or signs of wear.

Business outcome: Real estate firms and lenders can improve valuation accuracy, speed up mortgage and investment approvals. Our customers in the real estate sector were able to make more informed underwriting decisions in changing market conditions.

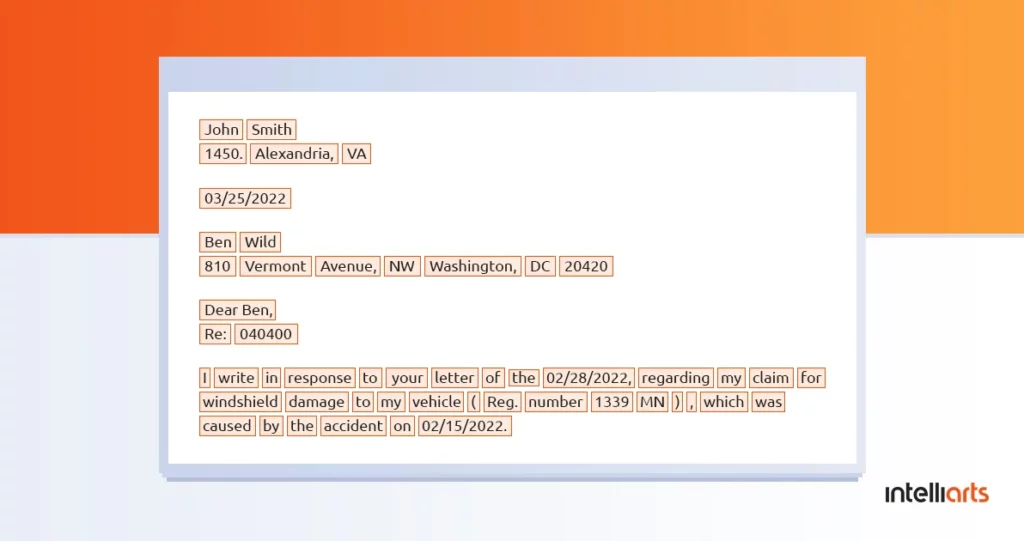

Intelligent document processing

Problem: Handling new underwriting submissions means going through volumes of documents within the shortest deadlines possible. As said, doing it manually takes not only lots of time but is inefficient and error-prone.

Automated data extraction: Optical character recognition

ML solution: AI underwriting platforms use OCR and NLP technologies to automatically extract, classify, and validate information from documents. ML-powered data pipelines can process applicant details, financial records, and asset information in real time.

Business outcome: ML-powered solutions give a chance to speed up submission processing. Instead of wasting time looking for underwriting information, such as an applicant’s names, addresses, risk types, or partner details, and entering it into the system manually, professionals can rely on fully automated systems to extract and organize data quickly and accurately.

Read also about automatic data extraction from DPFs.

Equipment / asset financing

Problem: Underwriting for leased equipment, vehicles, or industrial assets often involves fragmented operational data, inconsistent evaluations, and manual verification processes.

ML solution: In this sector, ML underwriting systems can analyze asset usage patterns, maintenance history, IoT data, and customer financial profiles to automate risk evaluation and optimize financing terms.

Business outcome: Leasing and financing providers can reduce manual workload, improve asset risk visibility, and deliver faster, more personalized financing decisions to customers.

Automating submission triaging

Problem: Underwriting teams often spend lots of time manually sorting, categorizing, and routing submissions to the appropriate specialists. As application volumes grow, this creates operational bottlenecks and delays in decision-making.

ML solution: Predictive underwriting contributes to creating a more efficient working model as ML helps to prioritize submissions based on different factors and make sure that a particular application will be handled faster. For example, an ML system can filter the applications based on their complexity and assign them for review to the underwriter with the appropriate level of knowledge. Another example includes prioritizing submissions by category, such as loans, leases, or policy types, and routing them to specialists with relevant domain knowledge for faster and more accurate evaluation.

Business outcome: Organizations can reduce review delays, improve workflow efficiency, and allow underwriters to focus on complex assessments instead of manual sorting tasks.

Challenges and risks of machine learning underwriting

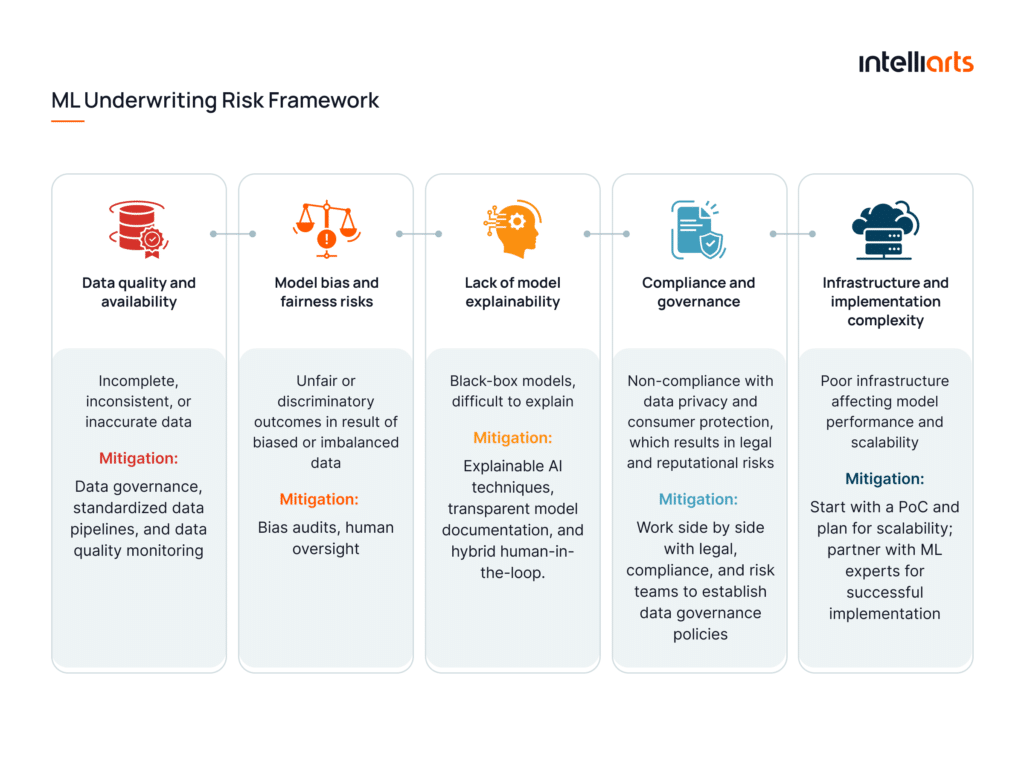

While machine learning underwriting can significantly improve efficiency, our partners know first-hand that its implementation also introduces a range of technical, operational, and regulatory challenges that have to be addressed properly:

Data quality and availability

The effectiveness of ML algorithms depends on data. And this must be quality data, without duplicates, null, and missing values. Data fuels ML not only as the “training material” but a way to make the models smarter in the future.

Mitigation: Invest in data governance, standardized data pipelines, and ongoing data quality monitoring before scaling ML underwriting initiatives.

Model bias and fairness risks

Machine learning models can unintentionally inherit biases from historical underwriting decisions or imbalanced datasets, potentially leading to unfair or inconsistent outcomes.

Mitigation: Implement bias audits and human oversight processes to evaluate model behavior and reduce discriminatory outcomes.

Lack of model explainability

Complex ML models can make underwriting decisions difficult to interpret, especially in highly regulated industries where businesses must justify approvals, denials, or pricing decisions.

Mitigation: Use explainable AI techniques, transparent model documentation, and hybrid human-in-the-loop.

Regulatory and compliance constraints

AI underwriting systems must comply with evolving regulations related to data privacy and consumer protection. Requirements such as CCPA, CFPB fair lending guidance, and emerging AI governance frameworks create additional compliance complexity for enterprises operating in the US market.

Mitigation: Contact legal, compliance, and risk teams early and involve them in the implementation process to establish governance policies for model monitoring, auditability, and data usage.

Infrastructure and implementation complexity

Implementing and scaling machine learning underwriting requires more than building ML models. Businesses also need reliable infrastructure for data storage, model deployment, monitoring, retraining, and integration with existing underwriting systems.

Mitigation: Start with a focused proof of concept (PoC) before expanding into production-scale underwriting automation. Furthermore, think in advance (or better discuss with ML experts) where to store and how to manage data in a productive way.

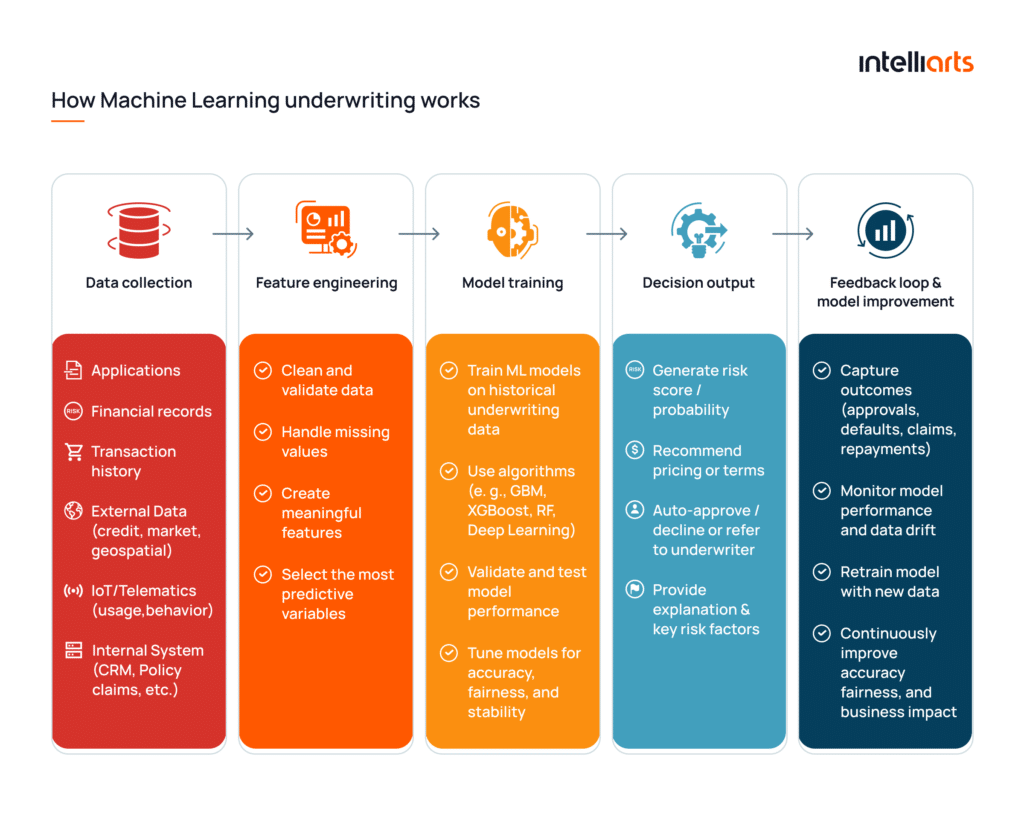

How machine learning underwriting works

Working with AI/ML models for over 5 years, we know that underwriting automation follows a structured workflow that transforms raw data into automated, data-driven decisions. While implementations vary across industries, most ML underwriting systems follow the same core pipeline:

- Data collection: The system gathers structured and unstructured data from multiple sources, such as applications, financial records, transaction history, property data, IoT devices, public databases, and internal business systems.

- Feature engineering: Raw data is cleaned, standardized, and transformed into meaningful variables (“features”) that ML models can analyze. This step helps identify patterns related to risk, fraud, pricing, or applicant behavior.

- Model training: ML models are trained on historical underwriting and outcome data to learn how different variables influence approvals, defaults, claims, or asset performance. This is an iterative process, and the system continuously improves as more data becomes available.

- Decision output: Once trained, the underwriting model generates predictions, risk scores, pricing recommendations, or approval decisions in real time. High-risk or ambiguous cases can be automatically escalated to human underwriters for review.

- Feedback loop and retraining: Modern systems continuously monitor outcomes and retrain models using new operational data. This feedback loop helps improve prediction accuracy and reduce model drift over time.

Now let’s consider what businesses need to know to implement AI underwriting the most efficiently.

How to implement machine learning underwriting

Some leads come to us being sure that building ML models is all they need. In reality, successful machine learning underwriting implementation goes beyond the solution itself: it’s your chosen strategy, data infrastructure, and close collaboration between technical and domain teams.

Here are a couple of things that you should know before even starting to look for a vendor:

Timeline

Most ML underwriting initiatives begin with a PoC targeting a single workflow such as submission triaging, risk scoring, or document processing. Once the business impact is validated, you can gradually scale the system.

A typical implementation timeline looks like this:

- PoC: 6–10 weeks

- Model development: 2–4 months

- Deployment and optimization: ongoing iterative improvement

Starting with a smaller use case helps businesses reduce implementation risks, validate ROI faster, and establish governance processes before scaling the solution.

Team roles

Effective underwriting automation projects usually involve both technical and business stakeholders:

- Data scientists build and optimize ML underwriting models

- ML engineers manage deployment, monitoring, and retraining pipelines

- Data engineers prepare and maintain underwriting data infrastructure

- Domain experts and underwriters validate business logic, risk policies, and decision quality

- Compliance and legal teams ensure regulatory alignment and auditability

Pro tip: Experienced AI consulting and implementation teams like Intelliarts can often cover multiple roles simultaneously. For example, senior ML experts with domain expertise in underwriting can contribute to model development and infrastructure planning at the same time. This allows our partners to speed up implementation while reducing coordination overhead.

Data requirements

As said, the performance of machine learning underwriting depends heavily on data quality and accessibility. Most underwriting businesses use a combination of:

- Historical underwriting decisions

- Claims or repayment outcomes

- Financial and operational records

- CRM and application data

- Third-party risk and market data

As our experience proved us, you do not necessarily need perfect datasets to begin. But do pay attention to reliable data governance and consistent formatting. Scalable data pipelines are a great advantage too.

KPIs to measure success

Think ahead of how you’re going to evaluate AI underwriting performance. Typical KPIs usually include:

- Underwriting turnaround time

- Approval processing speed

- Risk prediction accuracy

- Manual review reduction

- Underwriting cost per application

- Customer conversion rate

- Loss ratio or default rate

In Intelliarts’ experience, companies that define measurable KPIs early in the implementation process are more likely to scale underwriting automation successfully and demonstrate clear ROI to stakeholders.

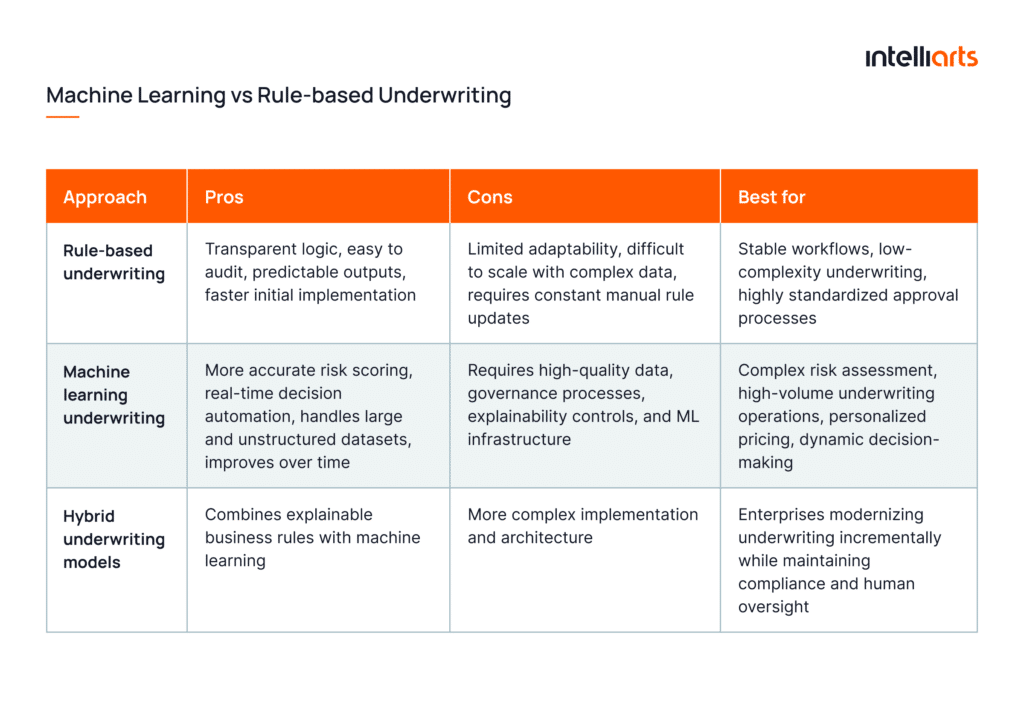

Machine learning vs rule-based underwriting

Both machine learning underwriting and rule-based underwriting aim to automate decision-making, but they differ significantly in flexibility, scalability, and risk analysis capabilities:

- Rule-based systems rely on predefined logic and thresholds

- ML underwriting continuously learns from historical and real-time data to improve predictions and decision accuracy

Many of our clients choose to adopt hybrid underwriting approaches that combine rule-based governance with ML-powered risk analysis. This allows to improve underwriting efficiency and scalability while also maintaining transparency and regulatory control.

Rule-based underwriting gives you control and predictability, while machine learning adds to adaptability and deeper risk intelligence. In our experience, the strongest underwriting systems combine both approaches, using business rules for governance and ML models for faster, data-driven decisions. – Volodymyr Mudryi, Data Scientist at Intelliarts

Regulatory and compliance considerations

Regulatory compliance is especially important in industries such as insurance, lending, real estate, and financial services, where underwriting decisions directly affect customers and business risk exposure. So businesses must ensure their ML systems comply with:

- CCPA (California Consumer Privacy Act): If you operate in the US market, your company must comply with data privacy regulations governing how personal information is collected, processed, stored, and shared. Since ML underwriting systems often rely on large volumes of customer and operational data, it’s essential to stick to transparent data governance and consent management.

- CFPB Fair Lending Guidance: In lending and credit underwriting, the Consumer Financial Protection Bureau (CFPB) requires to make sure that automated underwriting does not result in discriminatory outcomes. Businesses must be able to explain underwriting decisions and demonstrate fairness across customer groups.

- NAIC AI Governance Principles: The National Association of Insurance Commissioners (NAIC) provides guidance for insurers implementing AI systems, focusing on transparency, accountability, data governance, and risk management.

- EU AI Act: Companies operating internationally should also monitor the EU AI Act. The latter introduces risk-based governance requirements for AI systems, including transparency, documentation, monitoring, and human oversight for high-risk decision-making apps.

Need a compliant AI underwriting solution? We provide insurance underwriting software development services for those looking to modernize legacy underwriting workflows, improve regulatory compliance, and implement scalable AI-driven decision automation.

Real-world machine learning underwriting example

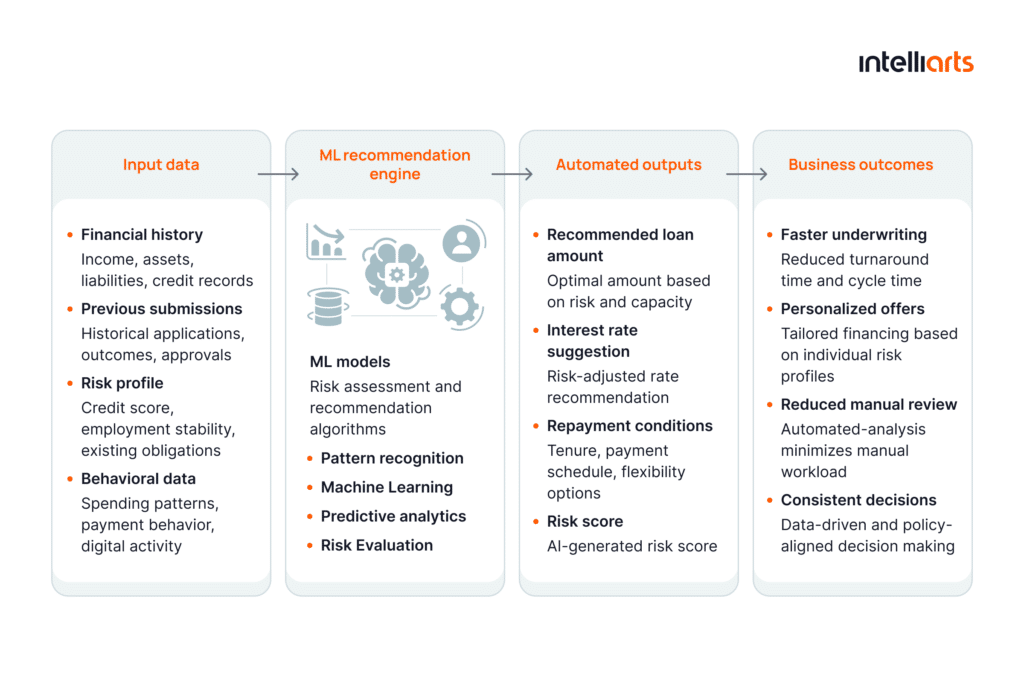

At Intelliarts, we worked on an ML-based underwriting recommendation engine designed to help improve coverage and financing recommendations through predictive analytics and decision automation.

Problem: An insurance company (under NDA) operated in a data-intensive underwriting and needed a faster and more personalized way to evaluate applicants and recommend appropriate financing conditions. In their workflow, our partner relied on manual reviews and static decision rules, so it was impossible to adapt recommendations to individual customer risk profiles and financial behavior.

As application volumes increased, the underwriters struggled to consistently determine the most suitable loan amounts, interest rates, and repayment conditions for each applicant.

Solution: The Intelliarts team developed an ML-based recommendation engine designed to support underwriting decisions using historical underwriting data and previous submission outcomes. The system analyzed applicant financial history, behavioral patterns, and risk profiles to predict the most appropriate financing and coverage recommendations automatically.

Outcome: After the solution was implemented, the company improved the consistency and speed of underwriting recommendations. Also, the engine reduced manual decision-making effort, and the underwriters were able to process applications faster and deliver more personalized financing conditions.

Empowering underwriters with machine learning

With businesses across industries dealing with growing volumes of data and undergoing digital transformation, more organizations recognize the merits of implementing AI and ML solutions. Teams responsible for evaluation and decision-making like underwriters can especially win on machine learning for underwriting by:

- Prioritizing submissions and assigning them to the most appropriate specialists

- Processing documents during the application review faster and more efficiently

- Calculating risks more accurately

- And giving personalized offers to their clients

Getting started with machine learning underwriting can be challenging, though. In case your company is looking for a professional team for the full-scale development of an ML-based underwriting system, we are ready to assist. Working according to the CRISP-DM methodology, we take an all-around approach to software solution development.

FAQ

What is machine learning underwriting?

Machine learning underwriting uses AI and ML models to automate risk assessment, application review, pricing, and decision-making across industries such as insurance, lending, real estate, and equipment financing.

How does ML underwriting differ from a traditional automated underwriting system (AUS)?

Traditional automated underwriting systems rely on static rules and predefined logic, while ML uses predictive models that continuously learn from historical and real-time data to improve outcomes (risk scoring, decision accuracy, etc.).

What ROI can a business expect from ML underwriting, and how is it measured?

Businesses typically measure ML underwriting ROI through faster approval times, reduced manual review workload, improved risk accuracy, lower operational costs, and higher customer conversion rates.